Unraveling the Mystery of Covered vs. Non-Covered Securities on the IRS Form 1099-B

March 19, 2024 10:00 AM MST

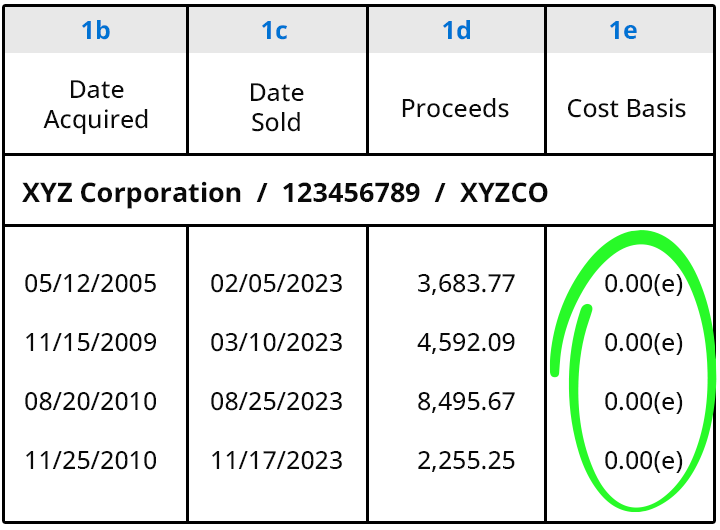

Unfortunately, a large number of investors receive 1099-B forms that only provide a portion of the investment information needed to complete the IRS Capital Gains & Losses, Schedule D form. The adjusted cost basis is provided for “covered” securities, but the “non-covered” securities section is left at zero. This often creates confusion for taxpayers as to the difference between the two and exactly whether they are responsible for the non-covered securities. To start, understanding the definition of covered and non-covered securities is important for accurate tax reporting and compliance with IRS regulations.

1. Definition

- Covered Securities - Brokerage firms are required to report the adjusted cost basis for specific taxable securities, to the investor and the IRS on Form 1099-B.

-

Non-Covered Securities - Brokerage firms are not required to report the adjusted cost basis for non-covered securities to investors and to the IRS.

2. Effective Date

- Covered Securities - As a part of the Emergency Economic Stabilization Act of 2008, shares of common and preferred stocks, ETFs or ADRs are covered, if acquired on or after January 1, 2011. On the other hand, mutual funds are covered on or after January 1, 2012. Therefore the adjusted cost basis for investments purchased on the effective dates going forward are provided on the 1099-B form.

-

Non-Covered Securities - Securities acquired before January 1, 2011 and 2012 respectively, are considered as non-covered. Therefore the adjusted cost basis for investments purchased prior to these effective dates is not provided on the 1099-B form.

3. Broker Reporting Responsibility

- Covered Securities - Brokers are required to report the adjusted cost basis, sale proceeds, and short or long-term gains or losses.

-

Non-Covered Securities - Brokers are not obligated to provide any information on non-covered securities to investors or the IRS. However, the gross proceeds or redemption value from a sale may still be reported to the IRS.

4. Taxpayer's Responsibility

- Covered Securities - Even though brokers report cost basis information for covered securities, it is still the taxpayer's responsibility to ensure the accuracy of the adjusted cost basis and gain/loss information on their tax return.

-

Non-Covered Securities - Taxpayers are responsible for accurately calculating and reporting the adjusted cost basis and profit or loss from a sale of a security for non-covered securities on the IRS 8949 and 1120-S (Schedule D) form. Failure to do so could result in tax penalties.

5. How the Adjusted Cost Basis Impact Gain/Loss Reporting

- Covered Securities - Although brokers have provided the adjusted cost basis on the 1099-B for covered securities, taxpayers are still held accountable for the accuracy of what is reported on their taxes. Therefore, confirming the accuracy of this information prior to reporting it is important.

-

Non-Covered Securities - Since the adjusted cost basis is not provided for non-covered securities on the 1099-B, taxpayers must carefully calculate the adjusted cost basis in order to correctly report capital gains and losses on the IRS 8949 form.

6. Tax Reporting Forms

- Covered Securities - Information on covered securities is provided on Form 1099-B, which is provided to both the taxpayer and the IRS.

-

Non-Covered Securities - While brokers may still provide Form 1099-B for non-covered securities, the cost basis information will most likely be excluded and require the taxpayer to enter the correct and complete information on the IRS 8949 form.

Netbasis can help.

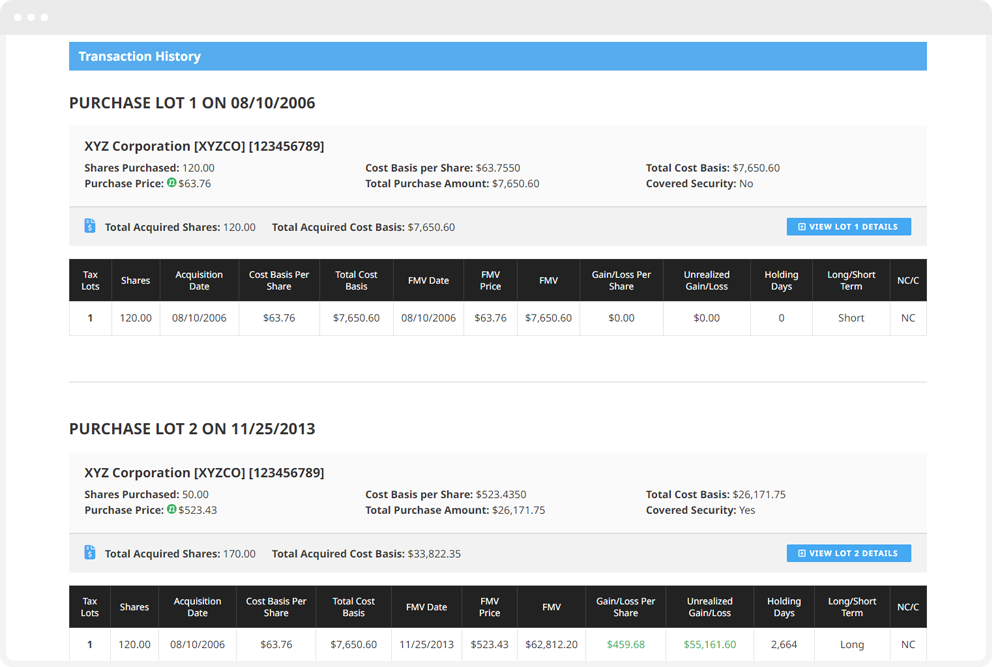

Netbasis, automatically calculates an adjusted cost basis for securities going back as far as 1925. Adjusting for all corporate events and dividends reinvested, Netbasis will generate a report that will provide the adjusted cost basis, long-term/short-term gain or loss, covered and non-covered shares, sales proceeds and fair market value.

POPULAR TOPICS

CRYPTOCURRENCIES

TAX MANAGEMENT